Good Buy or Goodbye (Again?)

Investors Debate Corn’s Value Signal

My usual modus operandi, also known as a method of operation, or simply “MO”, when putting these pieces together for my friends at Farmers Hot Line, I go back and look at what I wrote the previous year.

And sometimes, like this month, I find I could just copy and paste from one year to the next, as it fits with what I was thinking for the new piece. Either I’m caught in a cycle, the markets are, or possibly a little bit of both.

Watson Shifts Shape Market Positioning

This month, I was going to talk about King Corn’s seasonality, looking at the possibility of the market being a buying opportunity. Then I pulled up my piece for October 2024 titled, “Is Corn a Good Buy, Or a Goodbye?” The conclusion was the jury was still undecided, depending on what Watson (the algorithm driven investment industry) decided to do over the coming months.

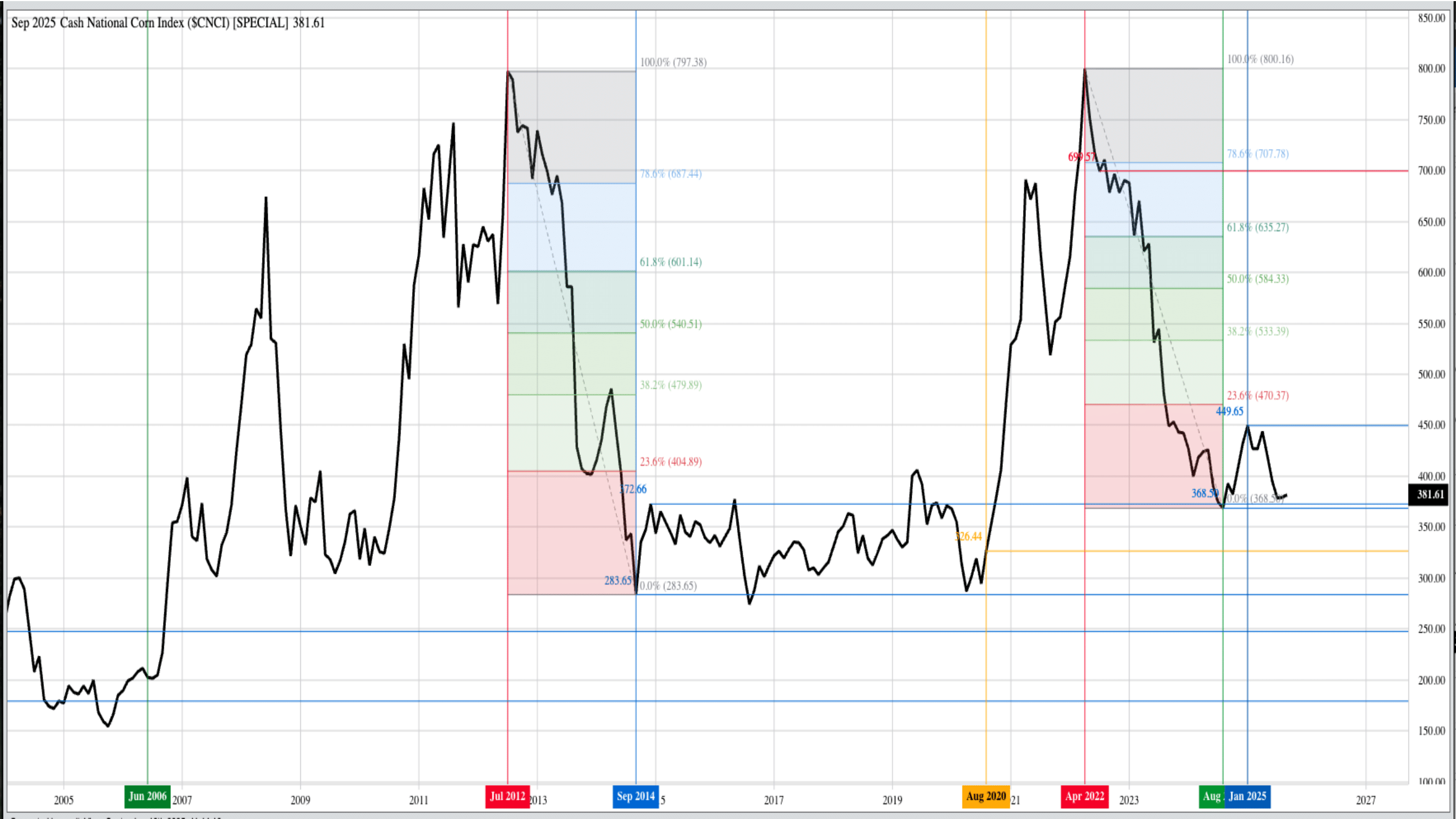

As it turned out, the corn market did rally with the National Corn Index (NCI, national average cash price) moving from a September 2024 settlement near $3.93 to a high monthly close in January 2025 near $4.50.

This move was driven in part by noncommercial buying with weekly Commodity Futures Trading Commission Commitments of Traders reports showing a switch from a net-short futures position (more short or sold contracts than long or bought contracts) of 266,000 contracts to a net-long (more long contracts than short contracts) of 468,000 contracts in mid-February 2025.

From there, though, Watson started selling, again switching to a net-short futures position of as much as 156,000 contracts as of July 1, 2025. This brought the NCI back to a low monthly close near $3.7850, within sight of the August 2024 settlement of $3.6850.

Indeed, the market does look to be in a cycle.

Funds Trim Shorts, Add to Longs

By early September, the noncommercial net-short futures position had been trimmed to 52,500 contracts, the smallest net-short futures position held by funds since late May. This decrease was the result of more than just short-covering (buying back short futures positions) as funds increased their long futures position by 63,450 contracts from July through September while decreasing short futures during the same time by 53,270 contracts.

This is an important distinction as it indicates the noncommercial side, including long-term investors in the market, viewed corn as a buying opportunity.

Why Investors See Opportunity Now

But why? I know, my own Market Rule no. 5 tells us, “It’s the what, not the why,” but in this case investors would need a reason to increase their position. With U.S. stock indexes continuing to hit new all-time highs over the course of the summer and early fall, new money is being generated to be invested in markets with bullish longer-term fundamentals. We’ve seen the cattle market find some of this interest as nearly every facet of the industry soared to new highs through early September.

Risk of the Poseidon Predicament

While providing incredible returns to investors, the move also increased the risk based on what I like to call the Poseidon Predicament.

This tells us that when everyone is on the same side of the boat, the boat tends to roll over. Again, why? Investors could start cashing in on some of the incredible returns seen over the past couple of years and move to the next market that looks to be a value opportunity.

Price Distribution Points to Value

I agree that corn looks to be a value investment. The NCI falling to its August 2025 settlement of $3.6850 put it in the lower 47% of its 10-year price distribution range, meaning slightly below the 50% level near $3.75.

While not indicating a solid buy, we have to keep in mind price distribution is but one of the filters in Market Rule no. 3: Use filters to manage risk, coming into play after we consider Rule no. 1 (Don’t get crossways with the trend) and Rule no. 2 (Let the market dictate your actions).

Long-Term Trend Still Points Higher

As I talked about last year at this time, the long-term trend of the corn market turned up at the end of August 2024, so we know investors will be looking for buying opportunities.

As August 2025 ended, the May 2026-July 2026 futures spread (price difference between contracts) covered a bullish 28% calculated full commercial carry. At the end of August 2024, the 2025 edition of this spread also covered 28%, again setting the stage for a similar fall/winter move in the corn market.

The bottom line is the corn market is in a similar position to where it was a year ago. While I do not believe in analogous years due to Chaos Theory, there is enough evidence as of this writing to conclude yes, investors could view corn as a good buy. We’ll see what happens over the next year.