The July Corn Countdown

Market Eyes Midwest Heat, Drought

When we think of July what’s the first thing that comes to mind? Many will likely respond “fireworks on the 4th,” though I lost interest in that celebration many years ago. Others will say lemonade and ice cream, both homemade to provide a break from the summer heat.

When it comes to grain markets, however, July tends to see the U.S. hard red winter (HRW) wheat harvest reach its peak leading to a seasonal selloff by the National HRW Wheat Index (national average cash price) that tends to extend through late August. Speaking of which, a look ahead to next month, known as the dog days of summer, and we see U.S. soybeans taking center stage. But this month belongs to the King of the Grains Sector based on the old saying, “Corn is made in July.”

Old-Crop Closes, New Begins

By the time you read this piece, the old-crop July futures contract will have moved into delivery, officially closing the book on interest in this past year’s supply and demand. Traders, both long-term investment and hedging interests, will have turned their attention to new-crop, and given grain markets are weather derivatives at heart, the spotlight will be on July’s weather. Now, I’m not a meteorologist, but I’ll make the forecast (confidently I might add), that July will be hot. How can I make this groundbreaking prediction? Because it is summer, meaning it is supposed to be hot, something most of the folks in the BRACE Industry (Brokers/Reporters/Analysts/Commentators/Economists) fail to realize as they scream at the top of their lungs about how catastrophic it is for crops. This wailing, gnashing of teeth, and rending of garments is as seasonal as the swallows returning to Capistrano in March.

Corn Supplies Outpacing Demand Trends

What might make 2025 different? At the end of May, the end of the third quarter of the 2024-2025 marketing year, the National Corn Index was priced at $4.20 putting available stocks-to-use at 12.6%. At the end of February, Q2 of the marketing year, the Index was $4.27 with available stocks-to-use at 12.4% meaning supplies of available corn had gained on demand over the past quarter. Additionally, the end of May 2025 available stocks-to-use figure was larger than the previous end of May average of 12.2%.

The significance of all these numbers is that the U.S. was on pace to have larger-than-average supplies on hand throughout the fourth quarter of the marketing year, with the 2025 harvest possibly starting in late July and picking up in earnest during August. Given this, it seems likely the Corn Index, like the previously mentioned HRW Wheat Index, will continue its seasonal downtrend this month.

Futures Spread Signals Planting Pace

What do we know about the 2025 corn crop as we turn the calendar page to July?

After tracking the November 2025 soybean/December 2025 corn futures contract from last September through February, it became clear that the corn market had attracted planted acres away from soybeans this spring. With that established, attention shifted to the September–December futures spread. Why? Because September is a hybrid contract — part old-crop, part new-crop — making its spread with December a useful indicator of spring planting progress.

This year, the spread posted a spring high close of 3.75 cents carry on March 10. From there, it declined sharply, reaching a low close of 16.75 cents carry by June 5. That growing carry suggests commercial traders were anticipating increased supplies — both leftover old-crop and early-harvested new-crop — being delivered against the September contract.

Commercial Carry Reveals Bearish Tilt

Digging deeper into the commercial outlook, let’s take a look at calculated full commercial carry (the percent covered by futures spreads, with the larger the number the more bearish/less bullish the fundamental outlook). At the end of May the new-crop December-July forward curve (series of futures spreads) covered a neutral 40% calculated full commercial carry. By late June the forward curve covered 42% indicating a slightly less bullish new-crop commercial outlook. A year ago, in late June, the 2024-2025 edition of the forward curve covered 32% before covering 42% the first week of July and 44% as the month came to an end. Could we see something similar occur this year? Most of the pieces seem to be in place, with one possible exception.

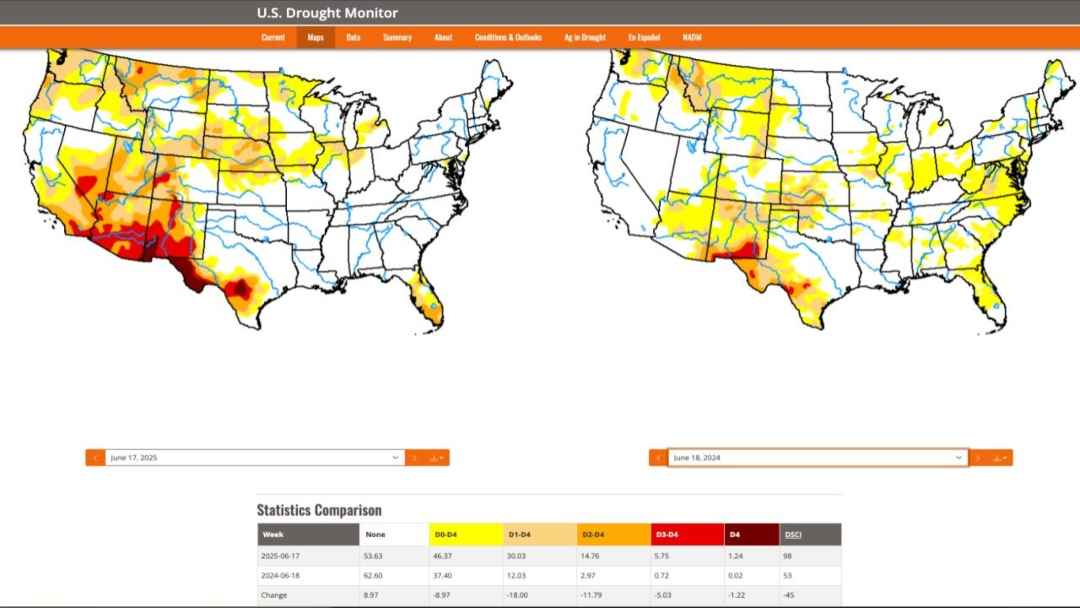

Dry Plains Add Market Pressure

The U.S. Drought Monitor map through mid-June 2025 showed deeper drought readings across the U.S. Plains and Midwest compared with the same week in 2024. In the Plains, the two states that stood out were South Dakota and Nebraska, the latter completely covered by drought to some degree. Last year, only two areas of slight concern appeared in Nebraska — the northwest and southeast corners.

Crossing the Missouri River — moving from the Plains to the Midwest — more abnormally dry areas (marked in yellow) were seen in Iowa. These two states could be key to the 2025 market as July approaches, if it proves to be the month the corn crop is made.

As of this writing, the market doesn’t appear overly concerned but is watching developing weather patterns closely. If conditions turn hotter and drier, fireworks — marketwise — could still erupt later this month.

About the Author

Darin Newsom has been working with markets in general for nearly 40 years, dating back to Black Monday 1987. Over that time, he has worked in local grain elevators, first dumping trucks then as a merchandiser, before becoming a commodity broker and advisor. That eventually led him to DTN where he spent 15 years as the company’s senior market analyst before going out on his own with Darin Newsom Analysis, Inc. These days, he also has the title of Senior Analyst for Barchart. Along the way, he has developed his own way of analyzing markets in every sector, always proudly reminding people that he is not an economist.